Founded in 2008, quant Global Research (qGR) is the thriving heart and inquisitive mind that energizes and guides the quant Group platform. qGR is driven by a simple idea: to extract predictive clues on market trends, it is critical to look beyond the obvious. Multiple data points outside the popular domain must be collected and synthesized into investment decisions using alternate analytical methodologies, as only differentiated research can lead to novel insights. A truism for all markets is that when everyone has found the key, the lock has already changed. Explore the unexplored. While following convention and staying with the herd may feel comfortable, markets do not follow what is written in textbooks.

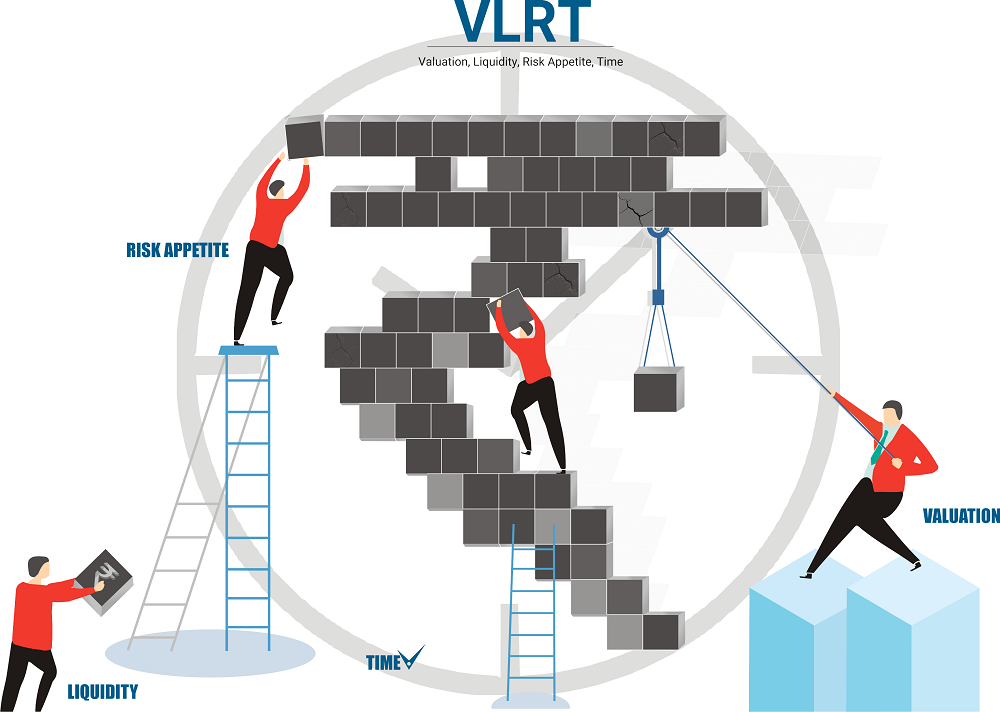

A decade ago, market research was focused primarily on the financial statements of a company, industry analysis and macro-economic studies to some extent. qGR began with a different idea about research with a focus on financial markets and the real economy as interlinked with feedback mechanisms, and a large emphasis on the role of investors’ dynamic behavior. This idea evolved into a multi-dimensional research perspective which is now formulated in our VLRT framework.

The ‘multi-dimensional’ aspects comes in because in addition to conventional qualitative analysis, qGR is extensively focused on quantitative measures and indicators of market patterns and various cash and derivatives market attributes. These diverse variables provide a picture of the inner workings and changing structure of various markets which form the ‘financial economy’. For the real economy, while formal economics is largely theoretical with assumptions-based models, qGR focuses on empirical market analysis, discovering a multitude of interlinked, overlapping though independently-driven cycles based on extensive historical data, going back centuries in some cases. Apart from cycles, pioneering research on global liquidity through alternate data sources enables quantification and tracking of the flow of money and its consequences across markets and asset classes.

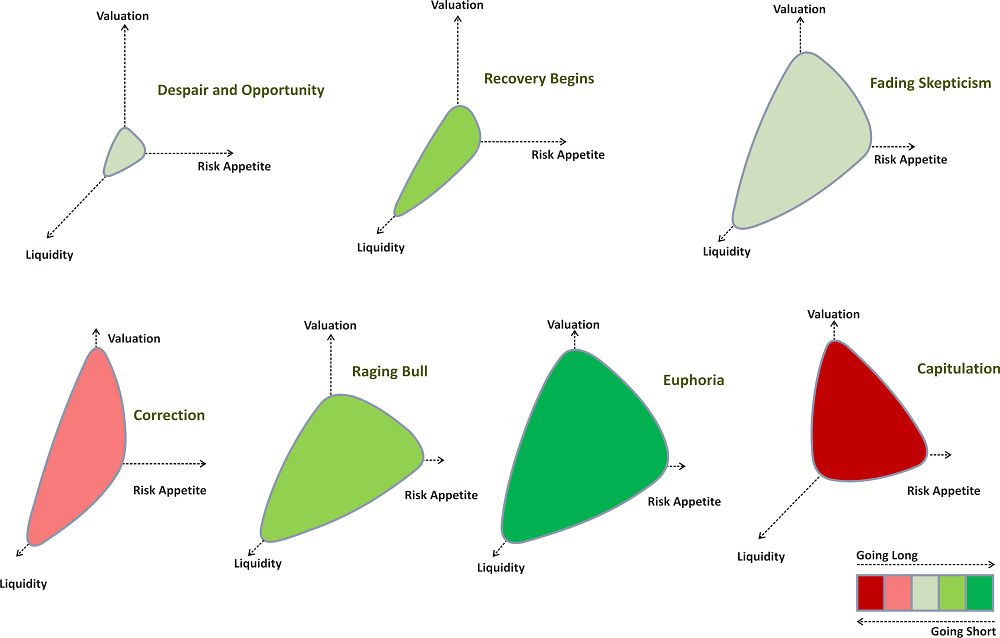

Going further, qGR behavioral analytics identifies the risk posturing of market and economic participants. The collective appetite of businesses and investors helps categorize the economic and market environment in zones of risk loving, neutral and risk aversion. Sentiment clues are also computed through proprietary risk indicators that enable us to quantify varying levels of fear and greed. Granular analysis specific to sectors or individual companies is also performed by identifying bouts of euphoria and panic.

Along with research, qGR provides a unique ‘Adaptive Asset Allocation’ execution methodology for money management. The various models, indicators and cycles are continuously being observed as they change with the market environment. Investment calls are triggered by certain observations in any one of the components, following which the call evolves based on further evidence from other relevant components. This endows our money management with an adaptive ability which we believe is the source of outperformance. There is no search for a Holy Grail, it is about applying simple and time-tested market logic through a multi-dimensional lens.

“quant’s indicators are unique in their ability to condense multi-dimensional research into a one-dimensional single number. Our typical day starts with quant Risk Index, one metric that encapsulates risk across markets and across assets. The challenge has been of marrying momentum with qualitative research, and assimilating various macroeconomic variables and time series data with cross-sectional data. It has worked well for us and we hope to continue our best efforts in that direction.”

– Sandeep Tandon

As Niels Bohr famously remarked, ‘it is very hard to make predictions, especially about the future”. Any market participant, whether a value investor or a day trader, would more or less agree with this statement. They would also agree that the task becomes exponentially more difficult with cross-asset, cross-market forecasts. As we go further out into the future, the cumulative amount of relationships and independent attributes that need to be analysed and predicted almost approach infinity.

As Niels Bohr famously remarked, ‘it is very hard to make predictions, especially about the future”. Any market participant, whether a value investor or a day trader, would more or less agree with this statement. They would also agree that the task becomes exponentially more difficult with cross-asset, cross-market forecasts. As we go further out into the future, the cumulative amount of relationships and independent attributes that need to be analysed and predicted almost approach infinity.

Yet, an honest attempt must be made and the analysis that we present to you here is the result of just such an attempt. A decade ago, we started out with a vision of the future that was substantially different than the prevailing perspective at that time. It gives us great pleasure to note that the past decade has seen the materialization of a substantial part of that thought process. To be honest, several mistakes have also been made but they are cherished by us even more as they helped us refine our tools and framework. At the same time, the diversity of research that we have covered has seen immense growth.

Now, at a crucial moment in history, we have formed another vision of the future after meticulously connecting the dots across a broad spectrum of phenomenon. We present here glimpses of that picture while being fully aware that it may not materialise completely. However, the glimpses we present here can serve as a rough map to navigate the uncertain future. The coming decades will be chaotic and overturn most of the commonly held beliefs and systems that we are accustomed to. Being prepared is the least we can do.

Words without action mean much less, of course, which is why we have embarked on a new journey with the launch of our money management business (quant Mutual Fund).

We believe it is the right time to test our philosophy, put on the glasses of our VLRT framework and implement the ‘Adaptive Asset Allocation’ methodology.

In a dynamic world, it is not just a choice but a necessity to adopt a multi-dimensional view.

We believe that alternate perspectives such as behavioral finance, volatility analytics and earth changes along with liquidity analytics are going to become more and more important.

The world is becoming non-linear and parabolic and to stay relevant, money managers must think with an unconstrained mind, actively update their methods and earnestly search for absolute returns, considering all markets and asset classes.